It is mid-June 2026. The NEET counseling madness is currently hitting its absolute peak. If you scored around 450 to 550, you are sitting in a very dangerous, uncomfortable zone. You check our competition analysis and realize you are thousands of ranks away from a free government seat.

But you desperately want the "Dr." tag. And your parents want it for you even more. So, the conversations start happening in the living room behind closed doors. You hear them talking about breaking fixed deposits. You hear them talking about visiting the bank to mortgage the ancestral land. You hear them talking about the "Management Quota" at a deemed medical university.

You feel a heavy mix of guilt and hope. You tell yourself, "It’s fine. Once I become a doctor, I will earn it all back and pay them off." I hear 18-year-olds say this all the time. It is a beautiful, naive sentiment. But it is fundamentally disconnected from the actual economics of the Indian healthcare system in 2026.

When you take a 1 Crore educational loan, you are not just borrowing money. You are mortgaging your entire 20s and a large chunk of your 30s. The bank does not care about your passion for saving lives. They care about compound interest. Let's completely strip away the emotion and look at the cold, hard numbers of what happens when you buy a private MBBS seat.

VRSAM Analytics: The 10-Year Debt Autopsy

Our educational research team at VRSAM tracked the historical changes made by the NTA over the last three exam cycles. Based on our evaluation of recent paper patterns, here is our custom blueprint for the 2026 syllabus.

To understand the financial trap, we must first break down the true Capital Expenditure (CapEx) of a private MBBS degree. In 2026, the advertised tuition fee for a management or deemed university seat typically ranges from ₹18 Lakhs to ₹25 Lakhs per annum. However, this is heavily deceptive. When our analytics team factors in mandatory hostel fees, mess charges, university examination fees, clinical material deposits, and miscellaneous annual hikes, the actual out-of-pocket expense consistently breaches the ₹1.1 Crore to ₹1.3 Crore mark over the 5.5-year duration of the course.

Assume a middle-class family secures an ₹80 Lakh educational loan, paying the remaining ₹30 Lakhs by liquidating lifetime savings. In 2026, unsecured loans are capped at ₹7.5 Lakhs. A loan of ₹80 Lakhs requires physical collateral—meaning the parents must legally mortgage their primary residence. The current floating interest rate for a secured educational loan sits at approximately 10.5% to 11.2%.

During the 5.5-year study period, the bank applies simple interest on the disbursed amounts. By the time the student finishes their internship and enters the mandatory 1-year moratorium period, the accrued interest alone adds roughly ₹25 Lakhs to the principal. The student is now staring at a total repayable burden of ₹1.05 Crores.

The financial reality violently collides with the clinical job market upon graduation. Our tracking of Junior Resident (JR) and Duty Medical Officer (DMO) salaries in corporate hospitals across Tier-1 hubs (Hyderabad, Bangalore, Chennai) reveals a stagnant pay scale. A fresh MBBS graduate in 2026 earns a median gross salary of ₹55,000 per month. In Tier-2 and Tier-3 nursing homes, this drops to ₹35,000 to ₹40,000.

Now, apply the debt math. To repay a ₹1.05 Crore loan over a standard 10-year tenure at 10.5% interest, the Equated Monthly Installment (EMI) mathematically strictly demands ₹1,41,000 per month.

The deficit is catastrophic. The young doctor is earning ₹55,000 while the bank is demanding ₹1.4 Lakhs. The graduate physically cannot service their own debt. The burden immediately falls back onto the parents, who are now typically entering their retirement age. They are forced to allocate their pension or continue working late into their 60s simply to prevent the bank from foreclosing on the family home.

Furthermore, this model assumes the student stops studying at the MBBS level. Our analytics show that less than 15% of private MBBS graduates are satisfied with a basic MBBS degree, as career progression without a specialization (MD/MS) is severely bottlenecked. If the student fails to secure a free government PG seat—which is statistically harder than the UG entrance—the family faces a second, exponentially worse financial crisis. Private clinical PG seats (like Radiology or General Medicine) currently command packages ranging from ₹1.5 Crores to ₹3 Crores. The family is mathematically destroyed.

The "I Will Work Hard and Earn it Back" Illusion

When I show this exact mathematical breakdown to 18-year-olds, they get defensive. They say, "Well, I’ll just work 80 hours a week. I'll do night shifts at multiple clinics."

Actually, let's play that out. You graduate at 24. You take a full-time 9-to-5 job at a corporate hospital earning 50k. To make extra money, you sign up for graveyard shifts at a small clinic from 10 PM to 6 AM. You are running on 3 hours of sleep. Your hands are shaking while trying to insert an IV line. You have absolutely zero personal life, no time for relationships, and your physical health starts decaying.

And even doing all of that, working yourself quite literally to the bone, you might bump your monthly income to 90k. You are still 50,000 rupees short of your EMI payment. You are running on a treadmill that is moving twice as fast as your legs can carry you. This is one of the most brutal common mistakes young students make: vastly overestimating the initial earning power of a basic MBBS degree in India.

The PG Bottleneck (The Final Boss)

We also need to talk about what happens five years from now. You bought the private seat. You survived the brutal MBBS exams. You finish your internship.

You walk into a hospital looking for a job as a physician. The hospital director looks at your resume and says, "Great, you have an MBBS. You can sit in the casualty ward and triage patients. We pay 45k." You look across the hall, and you see the Consultant Cardiologist (who has an MD and DM) charging ₹1,500 per 10-minute consultation.

You realize instantly that MBBS is just a baseline qualification now. It is basically the equivalent of a B.Tech. To actually get respect and high pay, you need a specialization. So, you have to write NEET PG.

Here is the problem: NEET PG is fundamentally harder than NEET UG. Why? Because you aren't competing against 18-year-old high school kids who don't know how to study. You are competing exclusively against 2 lakh other doctors. If you struggled to clear the UG cutoff, the PG cutoff is a nightmare. And if you don't get a government PG seat, a private MD Medicine seat costs another 1.5 Crores. Where is that money coming from when you still owe the bank 1 Crore from your UG days?

Emotional Blackmail vs Reality

The reason families fall into this trap is pure emotional blackmail. Indian parents will literally destroy their own financial security because they feel it is their "duty" to fulfill their child's dream. They will quietly sell the agricultural land. They will dip into their provident fund.

You are an adult now. You have to be the one to stop them. If your parents are incredibly wealthy business owners and 1 Crore is pocket change to them, go ahead. Buy the seat. Enjoy your life.

But if your dad is a salaried employee or a mid-level shop owner, do not let him take this loan. Look at the alternatives. Read our guide on BDS, BAMS, and Veterinary degrees where the ROI makes actual sense. Or take a drop year, isolate yourself, and study properly using the high-weightage chapters strategy. Do not ruin your family's next two decades over a title.

Frequently Asked Questions

What is the starting salary of an MBBS doctor in a private hospital in 2026?

In Tier-1 cities like Bangalore, Hyderabad, or Delhi, a fresh MBBS graduate working as a Duty Medical Officer (DMO) or Junior Resident makes roughly ₹45,000 to ₹65,000 per month. In smaller Tier-2 or Tier-3 towns, the lack of corporate infrastructure means the salary can drop to ₹35,000 depending on the hospital's bed capacity.

Are education loans easily available for a 1 Crore private medical seat?

No. Banks will not hand you 1 Crore just based on a college admission letter. For educational loans exceeding ₹7.5 Lakhs, banks mandate tangible collateral. To get a loan of this massive size, your parents will literally have to legally mortgage physical property (like your family home or commercial land) worth roughly the same amount. If you default, the bank takes your house.

If I take a private MBBS seat, can I easily clear NEET PG later to specialize?

No. NEET PG is statistically much harder to clear than NEET UG because the competition pool is exclusively composed of graduated doctors, not high school kids. The questions are deeply clinical. Many students who struggle with the UG cutoff also struggle to secure a free government PG seat, leaving them stuck with a basic MBBS or forcing them into another financial crisis.

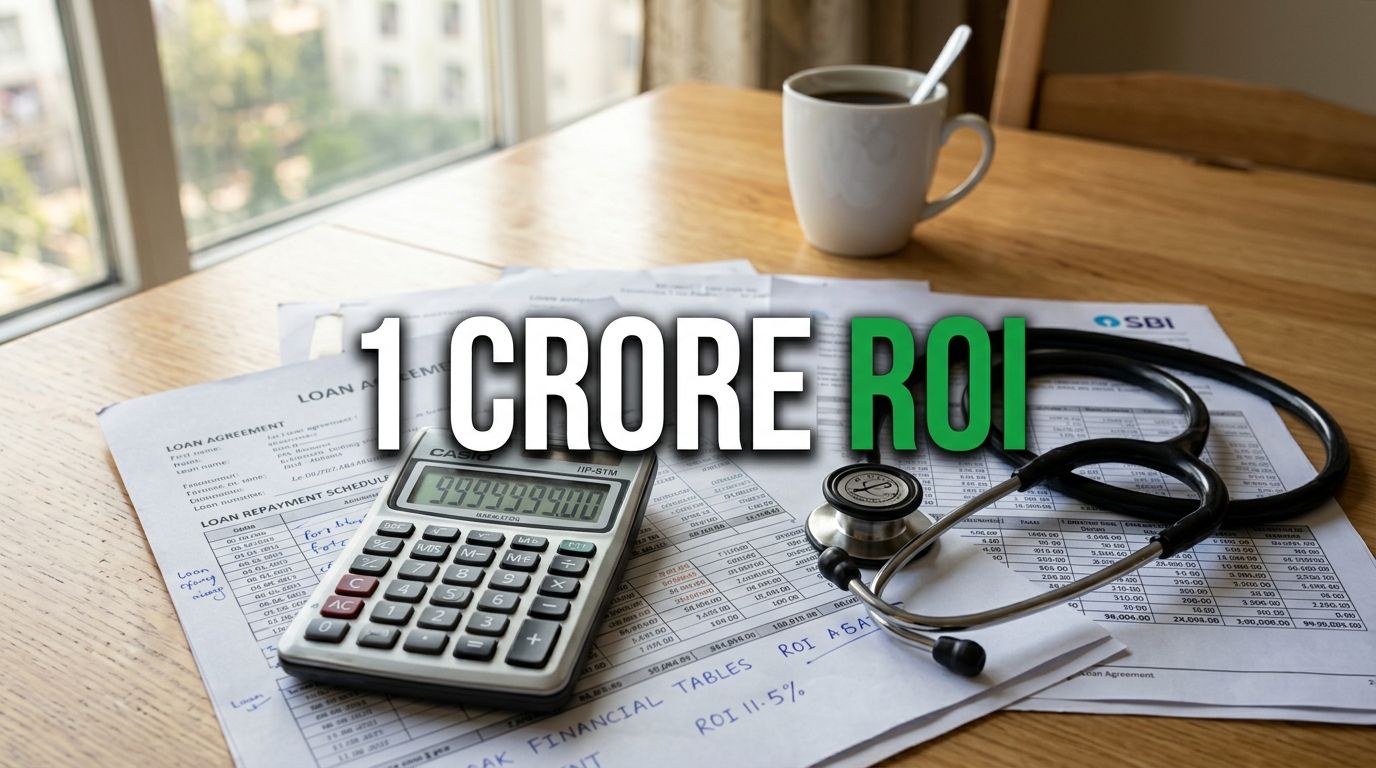

Go sit with your parents tonight. Open an online EMI calculator on your phone. Type in ₹1,00,00,000 at 10.5% interest for 10 years. Show them the monthly payment. Have the hard conversation now, before you are legally bound to a contract that you cannot escape.